Ask Ban Tacs

Ask Ban Tacs Question

- My Dad is the only member in the SMSF. He and I are the trustees. I have his power of attorney and I am the executor under his will. He is 87, and is declining.

- The SMSF has a real property asset worth circa $3M.

- Dad has put in place a non-lapsing BDBN, directing 100% of his super benefits to his estate.

- Dad’s current 2018 will specifically gives my brother the property. He is an adult non-dependent.

- Transfer costs (mainly stamp duty) if the property went to the estate and then to my brother would be approximately $150-200,000 (from the SMSF to the estate) then much less cost from estate to my brother.

- CGT is not an issue; there will not be a capital gain, but I do note if the property was transferred to my brother in-specie, he would have to wait 12 months before selling them to gain the 50% CGT discount.

- My brother is likely to want to sell the property, given that he resides a long way away, is on a disability pension and the property is not making money.

- Dad has not left my brother any money to pay for the transfer costs, or the death benefit taxes (another $100k or so), or to withstand losses for any reasonable period. My understanding is that the estate pays both the transfer costs and the death benefit taxes (unless the will specifies otherwise). Please assume the will provides that the beneficiary is to pay transfer costs and taxes.

- Dad is unlikely to get around to changing his will again to fix this.

- My understanding is that the estate will be responsible for paying the taxes payable on lump sum super death benefits. It will pay the taxes and deduct those from the beneficiaries’ payments? However, as Dad has not left my brother any money, how will the taxes be deducted if the properties are transferred in-specie?

- Dad could have the SMSF sell the properties before he dies, and he discusses that from time to time. In reality though, he is unlikely to do that.

My question is whether the Super Fund can sell the real property asset after Dad’s death, then give the net sale proceeds to Dad’s estate and then to my brother, instead of transferring those assets to the estate and then in-specie to my brother for him to then sell. I am relatively sure the Fund can do that before Dad dies, but my question is whether it can be done after he dies. That saves the transfer costs. If it is permitted, are there any relevant deadlines that might impact the idea? If any part of your answer depends on the Trust Deed wording, please just note that and we can look at that later. It allows transfer in-specie.

Answer

My initial answer is you can step into your Dad’s shoes after his death, for up to 6 months to wind up the SMSF and during that time it can stay in pension phase so no CGT on the sale of the property. I will get you more details on the fine print but might not be today. Is this the way you want to go? Should I just concentrate on the rules, processes and deadlines regarding the SMSF selling the property after your father’s

death?

Additional Information

That is astonishingly fast, Julia!

No need to answer today, take a week if you like. We must ease into the New Year.

CGT is not really an issue, but thanks for the advice. I am more focussed on the transfer costs and taxes, who pays them, how they get paid if no sale. You seem to have answered the bit about whether the SMSF can sell after Dad dies, even though the BDBN says to pay all benefits to the estate and the will specifically mentions the property. I guess from the estate point of view it is adeemed if sold by the SMSF.

Then yes, something about the rules, processes and deadlines regarding the SMSF selling the property after my father’s death would be great.

Hope that is clear enough.

Further Answer

Yes it is a great time of year to get a quick response. I am experiencing the same thing with other businesses, get in quick before all the Accountants come back on line.

BDBN pays all benefits to the estate – I trust there is nothing in the SMSF or BDBN that says this has to be inspecie. You might need to get legal advice on whether the will makes this happen by referring to him getting the property, but I doubt it as in public funds that can never be the case. Further beneficiaries can come to an agreement to divvy things up in the will differently without CGT consequences if no one actually pays anything for any asset they receive. I will rely on your legal advice as to whether you are executing the will correctly and move straight onto the whole selling the property in the SMSF issue.

References from NTAA 2016 Day 2 Super School notes

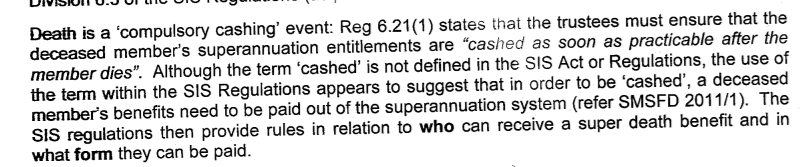

Need to Cash out benefit as soon as practical (BTW can be inspecie but you decided against that)

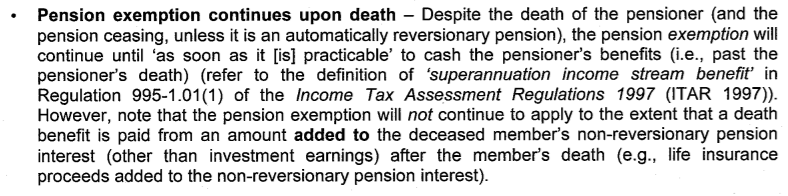

Best get the property sold and distributed in under 6 months to ensure no CGT

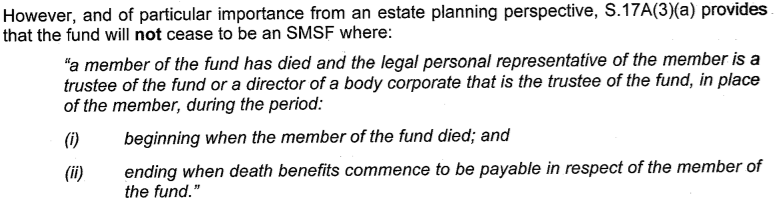

You need to take control of the SMSF or it will cease to be a fund

Process for the SMSF to pay the Estate

Process for the SMSF to pay the Estate

As the payment is being made to the estate the SMSF does not have to deduct tax or provide a PAYG summary. The estate is liable for the tax on the taxable portion.

The tax treatment of the death benefit payment is covered by section 302-140 and section 302-145: – The tax-free component (if any) is non-assessable non-exempt income and should not need to be reported on the tax return for the deceased estate; – The taxable component of the payment is included in the assessable income of the estate; – The trustee of the estate should be entitled to a tax offset to ensure that the rate of tax paid on the element taxed in the fund is capped at 15%; and – The trustee of the estate should be entitled to a tax offset to ensure that the rate of tax paid on the element untaxed in the fund is capped at 30%. When amounts are actually distributed to the beneficiary they should not report these amounts on their tax return as the tax has already been dealt with through the estate.